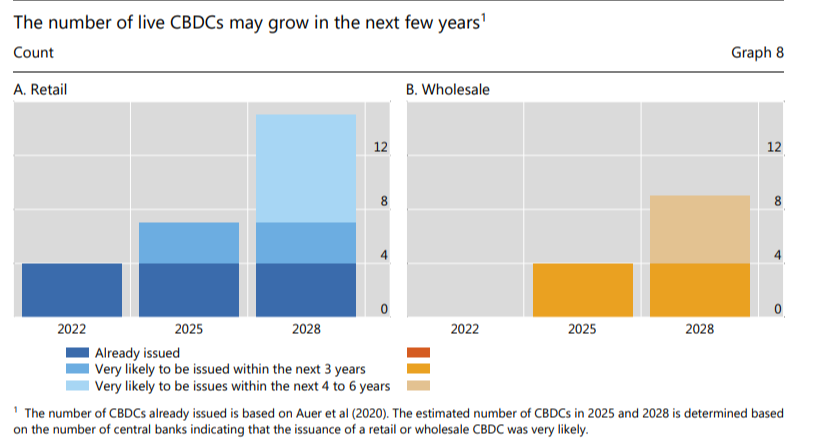

According to a survey by the Bank for International Settlements (BIS), 93% of central banks are researching central bank digital currencies (CBDCs). As per the report, by 2030, there could be as many as 15 retail and 9 wholesale CBDCs in circulation.

The survey of 86 central banks, published on July 10, took place from October to December 2022. It inquired whether central banks were working on retail, wholesale, or both forms of CBDC. They also accounted for the status of their work and their motivations.

A new era of finance with 24 CBDCs on the horizon

By the end of the decade, approximately two-dozen central banks in emergent and developed economies are anticipated to have digital currencies in circulation. In response to the accelerating decline of cash, central banks around the world have been researching and developing digital versions of their currencies for retail use to avoid leaving digital payments to the private sector.

Emerging markets and developing economy nations are geoeconomically at the forefront of CBDC adoption. Their participation in piloting the retail (29%) and wholesale (16%) digital currencies is nearly double that of developed economies, which stands at 18% and 10%, respectively.

AE and EMDE central banks are contemplating the issuance of a retail digital currencies for convergent reasons. In both AEs and EMDEs, domestic payments efficiency and payments safety have become nearly equally essential over time. AE and EMDE (AE = advanced economies; EMDE = emerging market and developing economies.) central banks place roughly equal emphasis on financial stability and efficacy of cross-border payments.

In 2022, the proportion of central banks that are projected to issue a retail digital currency within the next three years increased from 15% to 18%. At the same time, 68% of central banks are unwilling to issue a retail CBDC “anytime soon.”

There are now just four digital currencies in use: in the Bahamas, the Eastern Caribbean, Jamaica, and Nigeria. Nonetheless, based on central bankers’ responses, the survey estimates that 15 retail and 9 wholesale CBDCs will be operational by the end of this decade.

At the end of June, the Reserve Bank of India indicated that it was in talks with at least 18 central banks across the world about the prospect of making cross-border payments using its digital currency, the “digital rupee.” In July, the Innovation Centre of the Federal Reserve Bank of New York completed its proof-of-concept of a regulated liability network for a digital currency.

CBDCs set to take two different paths

As in prior years, central banks’ involvement in wholesale CBDC work is motivated by different incentives than their retail digital currency activities. In contrast to retail CBDCs, financial inclusion is the least major motivator of central banks’ efforts on wholesale digital currencies. Instead, the development of wholesale CBDC is motivated primarily by the aim to improve cross-border payments in both AEs and EMDEs.

The Dunbar initiative Dunbar, the findings of which were published in 2022, is an example of a cross-border wholesale digital currency initiative. The Reserve Bank of Australia, the Central Bank of Malaysia, the Monetary Authority of Singapore, the South African Reserve Bank, and the BIS Innovation Hub collaborated on this project to investigate how a shared platform for multi-CBDCs could enable cheaper, faster, and safer cross-border payments.

The likelihood of issuing a wholesale CBDC in the near future has also increased compared to last year: 16% of central banks believe it is likely that they will have a wholesale CBDC within the next three years, which is double the percentage of central banks from the previous year (8%).

In addition, 58% are likely or capable of issuing a bond in the medium term, up from 54% last year.27 Additionally, the likelihood of issuing a wholesale CBDC is generally greater in EMDEs compared to AEs.

According to the report, a legal framework granting central banks the authority to issue CBDCs is necessary for their issuance. The percentage of central banks with such legal authority increased marginally from 26% to 27% last year.

In addition, approximately 8% of jurisdictions are currently amending or clarifying their laws to allow it. During the second quarter of 2023, the European Commission intends to propose a regulation to establish a digital euro (ECB, 2023). Still, one-fourth of central banks lack the necessary legal foundation, and roughly forty percent are uncertain.

As the development of digital currencies progresses, central banks’ skepticism about short-term CBDC issuance fades. There is a distinct divergence: compared to last year. Some central banks are more likely to issue a retail CBDC within the next three years, while others are less likely.