The global economy is under fire. It’s not just inflation or supply chain issues. This time, the problem is bad politics and mounting debt.

Governments are racking up record debt, and political instability is a ticking time bomb for everyone. You’ve got the U.S. elections coming, war in Ukraine dragging on, tension in Taiwan, and chaos brewing in the Middle East. It’s all happening at the worst possible time.

Finance ministers and central bank chiefs are gathering this week in Washington for the International Monetary Fund (IMF) and World Bank meetings. But no one’s expecting much optimism.

IMF Managing Director Kristalina Georgieva says attendees will leave “uplifted, somewhat more scared,” hoping the fear drives them to take action. The outlook is bleak.

Political instability makes things worse

The U.S. election is a major factor in the global economic forecast. With two vastly different candidates, the stakes are high.

Donald Trump wants to impose a 10% tariff on all imports, with China getting hit even harder—up to 60%.

According to analysts Wendy Edelberg from the Brookings Institution and Maurice Obstfeld from the Peterson Institute for International Economics along with countless economists, Trump’s plan would wreak havoc on business.

Trump disagrees. He told Bloomberg:

“The higher the tariff, the more likely it is that the company will come into the United States and build a factory.”

But here’s the thing: if China retaliates, America’s GDP could drop by 0.8% by 2028, according to Bloomberg Economics. China wouldn’t get off easy, but the hit would be smaller at 0.4%.

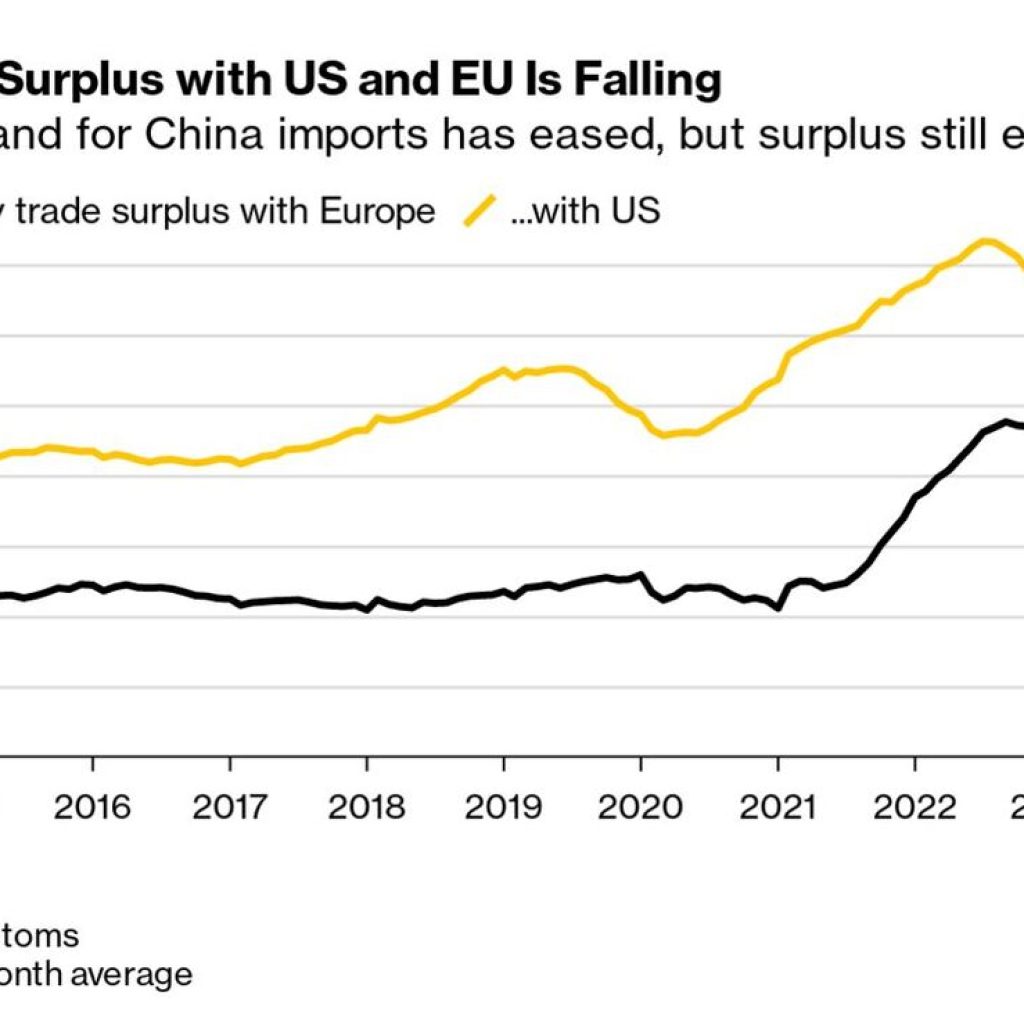

Europe, already struggling with weak demand and declining investment, could get caught in the crossfire, as cheap Chinese goods flood their markets.

The European Central Bank (ECB) has already lowered interest rates three times since June. Inflation seems to be cooling off, but ECB President Christine Lagarde isn’t celebrating.

“Any obstacles to trade matter for an economy like the European economy, which is very open,” she said, referring to Europe’s reliance on international trade. A new trade war would make things worse, and Europe’s fragile recovery could shatter.

While Europe battles with trade, America is dealing with its own problems. Consumer spending remains strong, and companies are still hiring, but government debt is climbing fast.

The U.S. Treasury reported that debt interest costs have hit a 28-year high due to rising interest rates and massive budget deficits. America isn’t alone in this.

The IMF predicts global public debt will reach $100 trillion by the end of the year. Governments are running out of options to fix the problem, and future recessions could leave them without the tools to respond effectively.

Wars and debt: A global disaster waiting to happen

Not just trade wars, but real wars are wreaking havoc too. Russia’s invasion of Ukraine is still ongoing, and the situation in the Middle East is getting worse.

Bloomberg Economics estimates that if a full-scale war breaks out in the Middle East, oil prices could hit $100 a barrel, shaving 0.5% off global growth and boosting inflation by 0.6%.

Higher oil prices mean everything gets more expensive, and countries already struggling with debt will feel the pain even more.

Meanwhile, China is trying to keep its economy afloat. The country’s growth has slowed, and the property sector is in trouble.

In response, Chinese policymakers have been rolling out stimulus measures daily, including cutting benchmark lending rates by 25 basis points. The one-year loan prime rate is now 3.1%, while the five-year rate is 3.6%.

These cuts are designed to boost corporate loans and household loans, with the hope of hitting China’s growth target of 5% this year. But the success of these measures remains uncertain.

Pan Gongsheng, the governor of China’s central bank, has also hinted at further cuts to the reserve requirement ratio (RRR), which dictates how much cash banks must keep on hand.

A reduction of 25 to 50 basis points could happen by year’s end, depending on liquidity. The seven-day reverse repurchase rate is set to be cut by 20 basis points, and the medium-term lending facility rate will drop by 30 basis points.

These are meant to support liquidity in the market, but they may not be enough to counteract the growing challenges facing China’s economy.

Bottomline is if governments don’t act fast, the situation could get much worse.