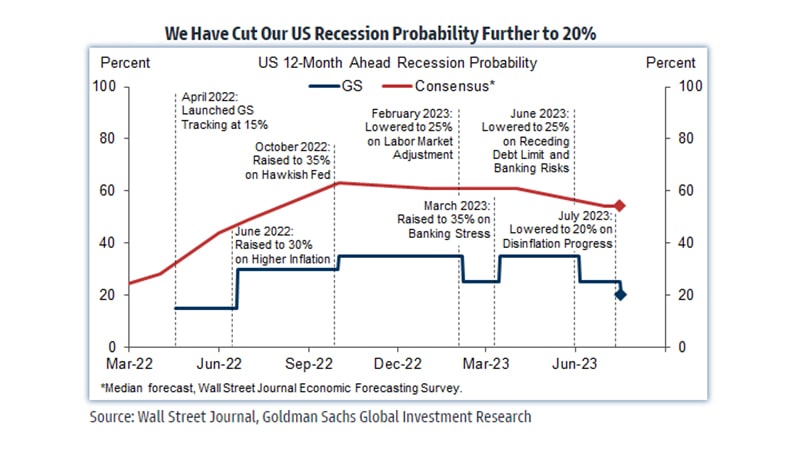

Goldman Sachs just tweaked its outlook for the U.S. economy, cutting the chance of a recession in the next year from 25% down to 20%. This comes on the back of solid retail sales data and lower-than-expected jobless claims.

The signals aren’t all rainbows and sunshine, but they’re good enough to make the economists at Goldman, led by Jan Hatzius, rethink the odds.

If the August jobs report, set to drop on September 6, doesn’t disappoint, they might cut that recession probability even further, potentially down to 15%. That’s where it sat comfortably before they bumped it up earlier this month.

U.S. economic indicators keep market on its toes

The latest batch of economic data has been enough to get Wall Street buzzing. Stocks had their best week of the year, driven by investors looking to scoop up bargains after a recent sell-off.

Retail sales in July showed a solid jump, the biggest since early 2023, signaling that consumers are still spending despite higher prices and borrowing costs.

That’s a good sign for the economy, considering consumer spending makes up a huge percentage of U.S. economic activity.

On top of that, fewer people filed for unemployment benefits last week than at any time since early July. That’s another sign the job market is holding up, even if job growth has been slowing down a bit.

But it’s worth noting that the job market still has some cracks. Nonfarm payrolls increased by 187,000 in July, which is below what experts had been expecting.

The Fed’s next move in the crosshairs

Goldman’s economists are also weighing in on what they think the Federal Reserve might do next. They’re becoming more confident that the Fed will cut interest rates by 25 basis points at their September meeting.

But, like everything else, it’s going to depend on the data. If the August jobs report comes with weaker-than-expected numbers, there’s still a chance the Fed might go for a 50 basis points cut instead.

The Fed has been in a tight spot, trying to balance the need to cool inflation without tanking the economy. Since March 2022, they’ve raised interest rates by 425 basis points, putting the federal funds rate in the 5.25% to 5.50% range.

These higher rates have been the main weapon against inflation, which, while moderating, is still above the Fed’s 2% target.

The Consumer Price Index (CPI) was at 3.2% as of July, while the Fed’s preferred inflation measure, the Personal Consumption Expenditures (PCE) Price Index, was at 2.8% in June.

The Fed’s aggressive rate hikes have brought back an old fear: the inverted yield curve. When short-term interest rates are higher than long-term rates, it’s often seen as a red flag for an upcoming recession.

The yield curve has been inverted since May 2022, and as of August 18, the spread between the 10-year and 2-year Treasury yields was -0.25 percentage points. Historically, this kind of inversion has been a pretty reliable recession predictor.

Despite Goldman Sachs trimming the recession odds, other models aren’t as optimistic. Some are still showing a 50-60% chance of a U.S. recession within the next year.

For example, the model from the Federal Reserve Bank of New York had the probability at 57.7% as of July. It’s based on a mix of economic indicators, including the yield curve.

Then there’s economist David Rosenberg’s view, which is even gloomier. He’s talking about an 85% chance of a recession in 2024, pointing to things like financial conditions indexes, debt-service ratios, and foreign term spreads.

Rosenberg’s take is that the combination of these factors is setting the stage for a huge slowdown.