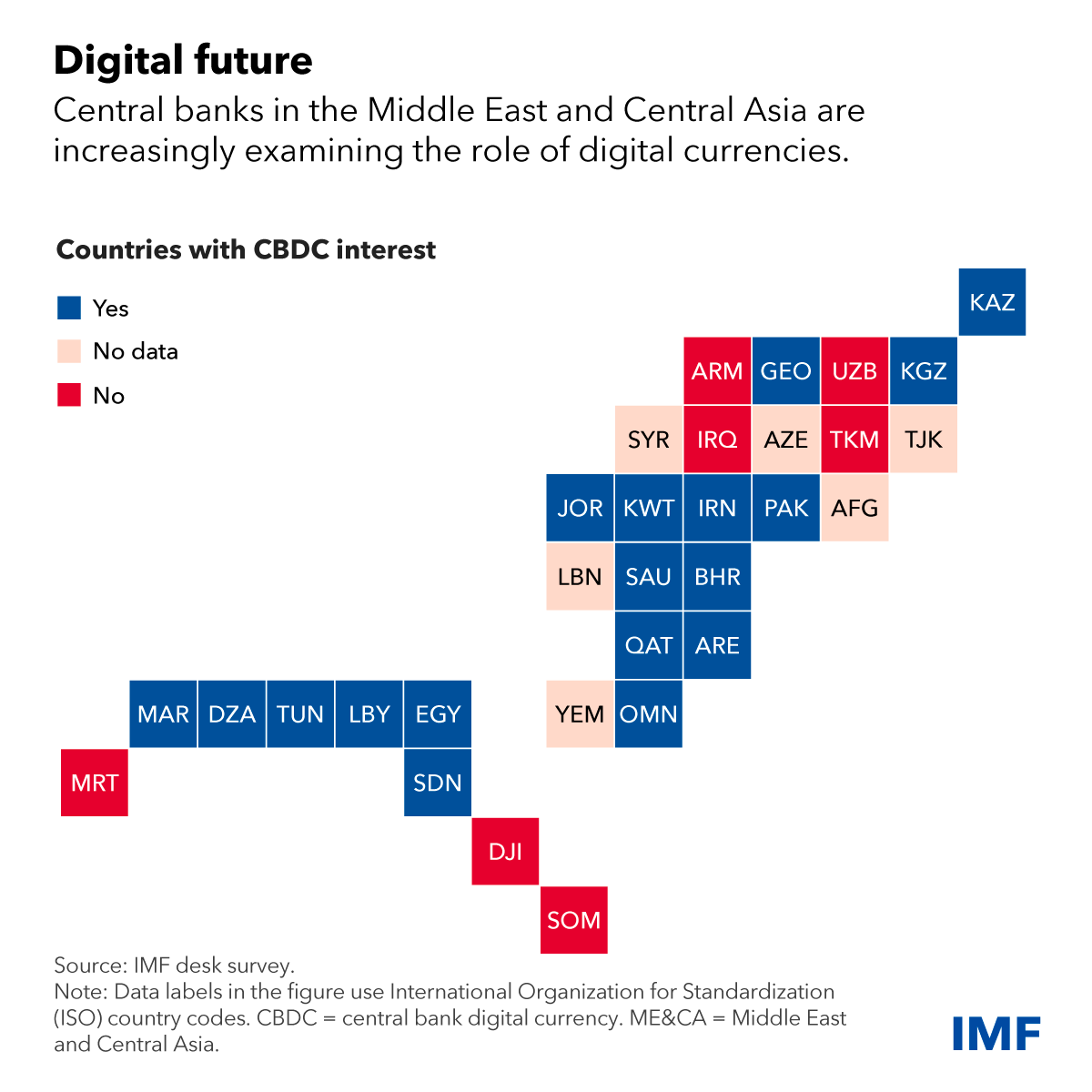

A survey conducted by the International Monetary Fund (IMF) of 19 central banks in the Middle East and Central Asia (ME&CA) region has found that central bank digital currencies (CBDCs) may not be necessary to achieve the intended policy goals. However, they can advance financial inclusion and lower the cost of financial services.

Also Read: SEC permanently ends all investigations into Ethereum

The IMF survey highlights CBDCs’ potential benefits in promoting financial inclusion and reducing the cost of financial services. However, it emphasizes the need for careful consideration when adopting a CBDC.

The IMF’s says CBDCs are good for ME&CA

The IMF has been carrying out extensive research on the evolution of CBDCs and providing guidance to member nations regarding their potential integration into their monetary systems.

The survey pointed out that addressing underlying constraints and enhancing other digital payment systems may be a more practical alternative to CBDCs.

Ultimately, introducing digital currencies will be a long and complicated process that central banks must approach with care [..] Policymakers need to determine if a CBDC serves their country’s objectives and whether the expected benefits outweigh the potential costs, risks for the financial system, and operational risks for the central bank.

The IMF

A senior IMF official has also mentioned the potential benefits of a global CBDC platform, highlighting, “one global CBDC platform that will allow for capital controls could cut payment costs.”

Several countries in the Middle East and Central Asia region, such as Saudi Arabia, have been considering the implementation of CBDCs. CBDCs have been proposed as potential replacements for cash in island economies, according to previous statements made by the IMF’s Managing Director Kristalina Georgieva.

CBDCs tap into the digital future

Several countries have already implemented cross-border technology platforms to tackle these concerns and encourage digital currency payments across borders. An example is the Buna cross-border payment system, which was established by the Arab Monetary Fund in 2020.

According to the IMF, central banks have the advantage of being able to keep costs lower since they are not driven by the need to make a profit, unlike commercial banks.

The heightened competition in the payments market due to a CBDC could drive the adoption of advanced technology platforms and enhance the efficiency of payment services, thereby expanding financial services to a wider audience.

This potential benefit is particularly sought after by countries in the Caucasus and Central Asia, Middle East and North Africa oil importers, and low-income countries.

CBDCs carry a danger policymakers should mitigate

According to the IMF, policymakers could mitigate potential risks to financial stability. IMF adds, “While there are no clear prerequisites to adopting CBDCs, a healthy banking system, a sound legal system, and strong supervisory and regulatory capacity are the most important for reducing risks.”

The survey shows that selecting the right features for CBDC implementation poses a significant challenge for regional policymakers. Successfully achieving the policy objectives of promoting financial inclusion and payment system efficiency will rely on making appropriate design choices.

For instance, designing CBDCs to work offline could promote financial inclusion in areas with spotty mobile service, such as in low-income countries and fragile and conflict-affected states. Similarly, using CBDCs for cross-border transfers could help lower the cost of sending remittances and speed up transfer times.”

IMF

As part of its efforts, the IMF is helping countries explore CBDCs. The entity states, “Through capacity development and surveillance, we support policymakers evaluating the need to issue a CBDC and help them craft strong policies and regulatory frameworks that can minimize monetary and financial stability risks.”

Also Read: Brazil summons top crypto exchanges to clarify their services

Lastly, the IMF is also publishing new chapters of its CBDC handbook. The entity has been guided by specific country capacity development questions on evaluating the needs and risks and developing concrete plans to issue a CBDC.

Cryptopolitan Reporting by Florence Muchai