WBTC’s discount dropped as low as -1.5% as questions swirled over whether WBTC is fully backed. Custodian BitGo later clarified that it is.

:format(jpg)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/6HAWVCX4EZHLBOECRI7UYPOANE.png)

The market contagion from crypto exchange FTX’s swift collapse has spread to a key digital asset: wrapped bitcoin, a widely traded clone of the largest cryptocurrency.

According to a new report from crypto analysis firm Kaiko, wrapped bitcoin (WBTC), the largest wrapped version of bitcoin on the Ethereum blockchain, has traded at a discount to bitcoin’s price since Sam Bankman-Fried's embattled FTX exchange filed for bankruptcy protection on Nov. 11.

Kaiko said WBTC’s discount dropped to as low as 1.5% Friday after investors reacted to questions posed on Twitter about whether WBTC is fully backed. The rumor was based on data from Messari's dashboard on Dune Analysis that says FTX’s sister company, Alameda Research, was a top WBTC merchant by the number of tokens minted.

Chen Fang, chief operating officer for BitGo, WBTC's official custodian, quickly clarified that every WBTC is “1:1 backed and verifiable on-chain.”

Friday’s rumors “appear to be unfounded” as Alameda would have needed to send all BTC to BitGo, meaning that the now-defunct exchange “never actually took custody of the BTC themselves,” the Kaiko report stated.

“Alameda was a ‘WBTC merchant,’ which means they’d accept BTC from customers and send it to BitGo to mint WBTC,” crypto influencer Udi Wertheimer tweeted. “Alameda NEVER custodied BTC themselves!”

Despite the clarification, WBTC’s discount is still at 0.5%, according to Kaiko.

Wrapped assets like WBTC are meant to be pegged to the value of the original asset. They are often used for trading, lending and borrowing on decentralized-finance (DeFi) platforms.

Bitcoin (BTC)’s price was recently trading at $16,143 Monday, while WBTC was changing hands at $16,112.

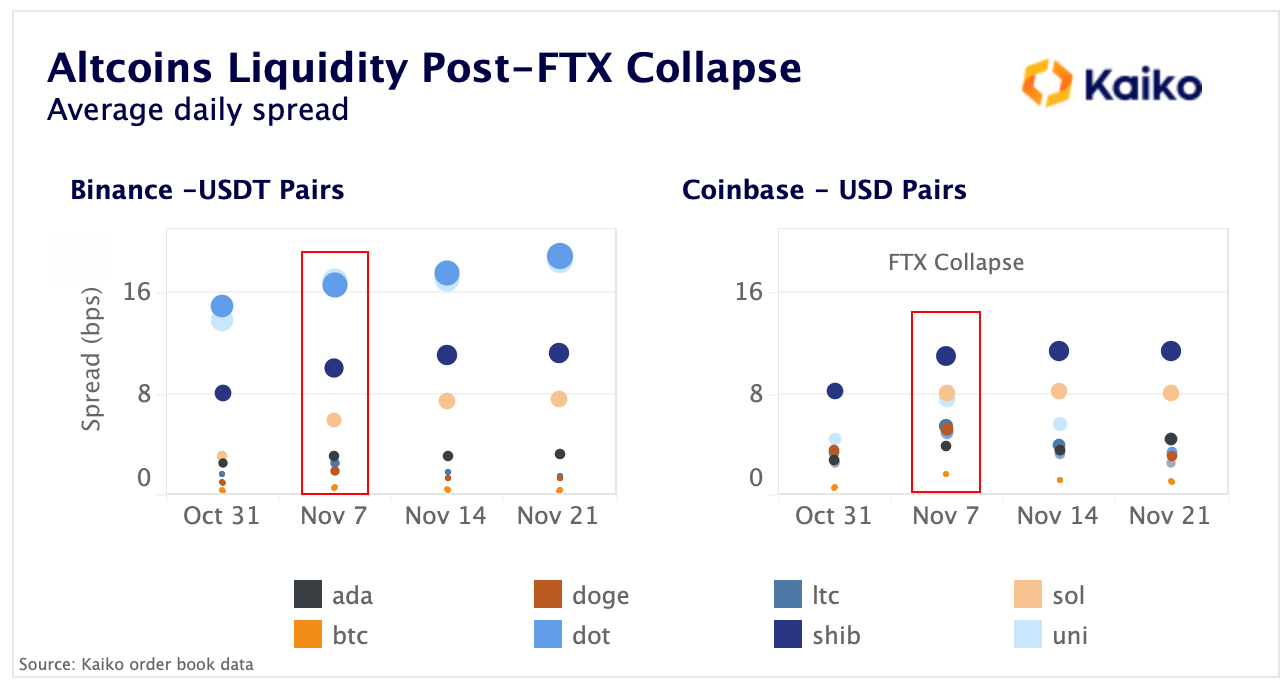

Altcoin liquidity worsens

FTX’s fallout gave birth to a phenomenon that Kaiko analysts previously have termed the “Alameda Gap” – a drop in liquidity across various crypto assets in the market, and altcoins’ liquidity took the hits more.

Kaiko said market makers are providing liquidity “asymmetrically, with spreads widening a lot more for higher-beta altcoins.”

By comparing the average daily spreads for the top altcoins by market cap on the Binance and Coinbase exchanges in the weeks before and after FTX filed for bankruptcy protection, Kaiko found that Solana’s SOL token had seen its spreads widen the most, “tripling from 2.1bps (basis points) to 7.4bps on Binance.”

SOL’s price has been falling sharply given its close ties with FTX/Alameda – plunging 59% in the past month. CoinDesk first reported on Alameda's balance sheet on Nov. 2 that the firm held $292 million of “unlocked SOL,” $863 million of “locked SOL” and $41 million of “SOL collateral.”

“Alameda was one of the most important market makers for some small-cap altcoins, while other major market makers registered losses and are likely to review their risk controls, which could impact liquidity in the short term,” the report from Kaiko said.